Table of Content

Your current wealth management platform wasn’t built for what your clients expect now. And rebuilding it is one of the highest-stakes technology decisions your firm will make.

Wealth management software development has moved beyond basic portfolio dashboards. Clients expect real-time consolidated views, AI-powered recommendations, and digital onboarding in minutes, not days. Firms that can’t deliver this are losing clients to those that can.

The global wealth management software market stands at $6.82 billion in 2026. It is projected to reach $11.82 billion by 2031 at an 11.63% CAGR, according to Mordor Intelligence. That is not a slow trend. That is an industry-wide sprint to modernize.

This guide gives your technology and strategy team a decision-ready framework. What to build. How to build it. What it costs. And how to get compliance right the first time.

| Dimension | Details |

| Market Size (2026) | $6.82 billion (Mordor Intelligence) |

| Projected Market Size (2031) | $11.82 billion at 11.63% CAGR |

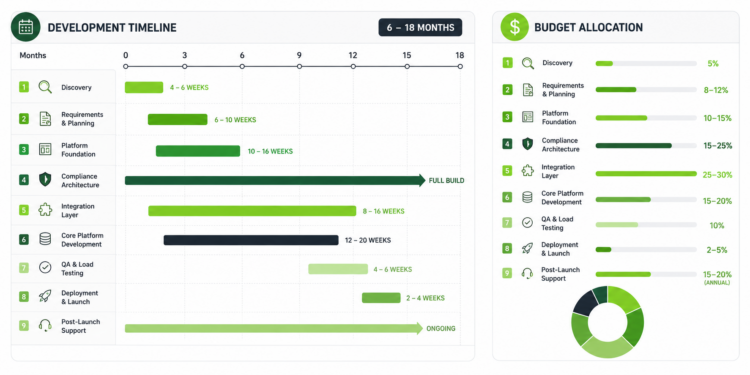

| Development Cost Range | $80K–$500K+ depending on compliance tier and integrations |

| Typical Build Timeline | 6–18 months (MVP to enterprise) |

| Primary Buyer Segments | RIAs, private banks, family offices, broker-dealers |

| Must-Have Integrations | Schwab, Fidelity, Pershing, Plaid, Bloomberg, Refinitiv |

| Compliance Frameworks | SEC Rule 17a-4, FINRA Rule 3310, KYC/AML, SOC 2 Type II, GDPR/CCPA |

| Top Technology Stack | Cloud-native (AWS/Azure), React/Angular, Python/Node.js, API-first |

| Key AI Applications | Portfolio analytics, hyper-personalization, automated rebalancing, NLP reporting |

| Build vs. Buy vs. Hybrid | Hybrid is the most common path for established firms modernizing an existing stack |

Sources: Mordor Intelligence (2026), Emerline (2026), 360 Research Reports (2025), Grand View Research (2024)

Most fintech development firms can ship features. Few have built financial platforms that operate under real regulatory constraints, serve millions of users, and hold up when the compliance scrutiny comes.

Code Brew Labs has done exactly that, across four regulated financial markets.

DuPay — Regulated Digital Wallet & Remittance Platform

Code Brew Labs built DuPay as a fully regulated digital payments app for the UAE market, one of the most compliance-intensive financial environments in the region.

The platform handles secure digital payments, local transfers, cross-border international remittances, and everyday bill payments; all within UAE financial regulatory requirements.

100K+ downloads. 4.8/5 average rating.

Building in the UAE meant handling multi-currency rails, regulatory KYC requirements, and real-time transaction processing from Day One. The compliance architecture wasn’t retrofitted. It was the foundation.

BharatPe — $600M+ Funded Merchant Fintech Platform

BharatPe is one of India’s most-funded fintech platforms, and Code Brew Labs built the technology behind it. The platform powers QR-based merchant payments, business loans, and digital bookkeeping for small businesses across India.

10M+ downloads. 4.7/5 average rating. $600M+ in funding raised.

At this scale, the engineering challenge is not the feature set. It’s the reliability, security, and regulatory compliance under high transaction volume. Code Brew Labs delivered infrastructure that investors, regulators, and 10 million users trust.

PostPe — Consumer Credit & Flexible Payments Platform

PostPe is a modern consumer finance platform offering flexible credit options and seamless payment services, built to simplify personal finance management at scale.

5M+ downloads. Available across platforms.

Building consumer credit products means KYC workflows, credit decisioning logic, and payment rails all have to work together without friction and without compliance gaps. Code Brew Labs built that stack.

ZeroPe — Medical Finance & Credit Solutions Platform

ZeroPe delivers credit and payment solutions purpose-built for healthcare needs, a vertical where financial trust, compliance, and UX precision are non-negotiable.

Live across platforms. Serving a market where financial product errors have direct human consequences.

This is the kind of build that sharpens compliance instincts fast. Code Brew Labs built the credit and payment architecture from the ground up.

| What this means for your wealth management platform: The compliance architecture, KYC workflow design, multi-currency rails, and regulated-market delivery experience across these four platforms directly transfer to wealth management software development. We didn’t learn financial-grade compliance on a client’s build. |

Also, watch our video:

Wealth management software is an integrated technology platform that enables financial advisors and institutions to manage client portfolios, deliver financial planning, automate compliance workflows, and give clients real-time visibility into their financial lives; all from one unified system.

It is not simply a reporting dashboard.

A purpose-built platform serves as the operational backbone for advisors. It is simultaneously a transparency tool for clients. It connects portfolio management, CRM, regulatory compliance, and financial planning into a single data model.

For established wealth firms, this distinction matters most: system of record versus collection of tools. The wrong choice creates friction. The right choice creates leverage.

Understanding what the software does is the starting point. The more important question is why 2026 is the year established firms are finally forced to act.

Approximately $84 trillion in assets will transfer between generations over the next 20 years (360 Research Reports). The recipients are digital-native.

They expect the same seamless digital experience from their wealth manager that they get from their bank or brokerage app. Firms built for the previous generation of clients are already misaligned.

In finance, nearly 50% of high-net-worth individuals under 45 would consider leaving for providers with better digital tools, such as robo-services. (PwC). The advisor relationship still matters.

But the platform experience is now table stakes. Advisors can’t save accounts that the technology is losing.

The industry is not waiting. According to 2025-2026 industry reports, the majority of financial institutions have increased their technology budgets to meet digital-first client expectations.

Firms that delay are not holding steady. They are falling behind peers who are already building.

45% of wealth managers now use some form of AI-driven analytics. Firms deploying automation report a 30% improvement in advisor efficiency from automated administrative tasks (The Wealth Mosaic).

The efficiency gap between digital and non-digital firms compounds every quarter it goes unaddressed.

Knowing why change is urgent doesn’t tell you what to build. The next section breaks down the components of a modern wealth management platform.

| Platform Type | Core Function | Best For | Key Examples |

| Portfolio Management Software | Tracking, rebalancing, performance analytics | RIAs, asset managers | Orion, Tamarac, Black Diamond |

| Robo-Advisory Platform | Algorithm-driven investment management | Digital-first firms, neobanks | Betterment for Advisors, SigFig |

| Financial Planning Software | Goal modeling, retirement, scenario analysis | Full-service advisors, private banks | eMoney Advisor, MoneyGuidePro |

| Risk & Compliance Systems | KYC/AML, audit trails, regulatory reporting | All regulated firms (mandatory) | Fenergo, Compliance, NICE Actimize |

| Client Portal & Communication | Real-time dashboards, secure messaging | Client-facing firms of all sizes | Orion, Envestnet, custom builds |

| Multi-Asset / Family Office Platforms | Private equity, real estate, collectibles | Family offices, UHNWIs | Addepar, Archway, custom enterprise |

| Custodian Integration Middleware | Data aggregation from Schwab, Fidelity, Pershing | Any multi-custodian firm | Plaid, Yodlee, proprietary API layers |

Sources: Mordor Intelligence (2026), Backbase (2026)

A modern wealth management platform is not a monolith. It is a set of interconnected modules, each serving a distinct operational function, that together create one unified experience for advisors and clients.

These are the six core modules your platform needs:

Consolidates data from multiple custodians, banks, and external data providers into a single, real-time view.

Without this, every other module is working from incomplete or stale data. This is the module that makes everything else accurate.

Handles portfolio construction, automated rebalancing, performance attribution, and tax-loss harvesting.

Advisors interact with this most throughout the trading day. It must be fast, accurate, and connected to live custodian data.

Enables advisors to run interactive “what-if” scenarios, model retirement outcomes, and visualize estate plans.

Clients engage with this directly through the client portal. It converts prospects and gives existing clients reasons to stay.

Manages KYC/AML screening, suitability checks, audit trail generation, and regulatory reporting. This module protects the firm from regulatory exposure. It must be built first, not added later.

This sequencing is where most firms make their most expensive mistake.

Gives clients 24/7 access to their portfolio performance, documents, and advisor messaging, without requiring a call. It is the primary driver of digital client satisfaction.

And it is the first thing a prospective client evaluates.

Powers hyper-personalized investment proposals, predictive cash flow analysis, and advisor next-best-action prompts. According to Mordor Intelligence (2026), generative AI copilots now draft meeting notes and rebalancing orders within seconds, freeing up 20–30% of staff time.

Feature lists are only useful when they distinguish between what every platform has and what the best platforms are built around. Here’s the difference.

Connecting to Schwab, Fidelity, Pershing, and Orion via API is not optional for any multi-custodian firm. This is the single most underestimated technical requirement in wealth platform builds.

Budget 20–30% of your total build cost for custodian integration alone.

The majority of clients now expect personalized investment strategies based on ESG criteria, personal values, and risk tolerance (Morgan Stanley).

Natural language processing engines now analyze 50+ data points per client interaction to deliver them. Platforms without this capability are already behind.

“What-if” tools, retirement outcome modeling, estate planning visualizations, tax projection scenarios, convert prospects, and retain HNWI clients.

Static PDFs are no longer acceptable. Clients who can model their own future stay engaged. Clients who can’t eventually leave.

Automated rebalancing maintains investment strategy without advisor intervention. Tax-loss harvesting adds quantifiable value clients can see on their statements.

It is a retention feature as much as a technical one. Firms that offer it have a clear, communicable differentiator.

Every client interaction, recommendation, and trade must be logged in a format that holds up under SEC or FINRA examination. This is not a logging feature.

It is a legal requirement that must be designed into the data architecture from the start, not configured as an afterthought after development is complete.

The shift from monolithic suites to modular, interoperable platforms means your platform must offer open API access to connect best-of-breed tools across the advisory stack. Lock-in to a single vendor’s feature roadmap is an architecture risk, not just a preference.

Family offices and international clients hold assets across private equity, real estate, collectibles, and multiple currencies.

Platforms built only for public market portfolios cannot serve this segment. And this segment controls the largest assets under management.

Most vendors give you two options: build custom or buy off-the-shelf. That binary misrepresents how seriously wealth firms actually make this decision.

The real question is: which components of your operational stack are genuinely differentiated, and which are commodities? Build what differentiates you. Buy or integrate what doesn’t.

| Criteria | Build Custom | Buy Off-the-Shelf | Hybrid (Build Core, Buy Modules) |

| Best For | Firms with unique advisory models, proprietary investment strategies | Firms needing rapid deployment, limited IT resources | Established firms modernizing an existing stack |

| Time to Market | 12–24 months | 2–6 months | 6–12 months |

| Upfront Cost | $200K–$500K+ | $50K–$150K/year (licensing) | $120K–$300K+ |

| Customization | Full | Limited by vendor roadmap | High on core, limited on purchased modules |

| Compliance Control | Full ownership | Dependent on vendor | Shared — critical to define clearly |

| Custodian Integration | Custom-built, full control | Varies by vendor | Often best handled in a custom core layer |

| Scalability | Built to your specifications | Constrained by vendor pricing | Scalable core; replace modules as needed |

| Vendor Lock-In Risk | None | High | Low to medium |

| Ideal Use Case | Family offices, private banks with proprietary strategies | RIAs seeking quick digitization | Most mid-to-large wealth firms |

Sources: Code Brew Labs analysis; Emerline (2026)

For most established wealth management firms, the hybrid path dominates. The compliance and data aggregation layers are too firm-specific to trust to a vendor’s roadmap.

Client-facing UX and financial planning modules, however, are strong candidates for best-of-breed procurement.

Once you’ve decided what to build, the question becomes how to build it without regulatory exposure.

Custodian integration is the most consequential technical decision in wealth management software development. Every other feature depends on it.

These four custodians collectively hold the majority of RIA-managed assets in the United States. Connecting to each requires dedicated API work, data normalization, and ongoing reconciliation logic.

Budget 20–30% of your total build cost for custodian integration alone if you are serving a multi-custodian book. This is not negotiable for any serious platform.

Real-time pricing, reference data, and alternative data feeds power portfolio analytics, performance reporting, and AI personalization engines.

These integrations are subscription-based with API layers that require careful rate-limit management and failover design. Skimping on this layer produces stale data, and stale data produces client complaints.

For platforms offering cash management, direct indexing, or alternative investment access, banking rail integration connects the wealth platform to the underlying financial system.

FDX API adoption is accelerating as the US open banking standard firms up. This is worth scoping early.

Modern wealth platforms use OAuth 2.0 for advisor tool integrations and SAML for enterprise SSO. Biometric liveness detection paired with OCR-based document capture can reduce onboarding from days to minutes, according to Garner (2026).

This is a client acquisition advantage, not just a technical specification.

For platforms connected to institutional trading desks or prime brokers, FIX protocol is the industry standard for order routing. Scope this explicitly in the architecture phase. Discovering it mid-build is expensive.

A pragmatic planning range:

15% to 25% of your total build budget goes to compliance architecture, once you account for legal readiness and technical controls (Emerline, 2026). Plan for it up front or pay 3–5× more to retrofit it later.

KYC/AML is simultaneously a client onboarding funnel and a regulatory obligation. Pairing biometric liveness detection with OCR-based document capture automates risk-scoring for low-risk customers in minutes.

The system must route exceptions to manual review and maintain a continuous screening audit trail. Both requirements must be built in, not bolted on.

For broker-dealers and registered investment advisers, SEC Rule 17a-4 mandates that electronic records be stored in a non-rewritable, non-erasable format (WORM storage) for specified retention periods.

This is a storage architecture requirement, not a logging configuration. It must be specified before a single line of code is written.

Broker-dealers must establish and maintain a written AML program under FINRA Rule 3310.

The platform’s transaction monitoring module must automatically generate Suspicious Activity Reports (SARs) required under this rule. This is a built-in system function, not a manual process.

Any platform handling client data will be asked for a SOC 2 Type II report by enterprise buyers.

Building SOC 2 readiness from Day One is dramatically cheaper than retrofitting it. It also reduces implementation timelines, which is a sales advantage, not just a compliance checkbox.

For firms serving European clients or California residents, data residency, right-to-erasure, and consent management must be built into the data model.

These are not features that can be added to a completed platform. They require architectural decisions made in the design phase.

A wealth management platform is not built like a standard SaaS product. Each phase carries regulatory and financial data implications that standard development processes aren’t designed to handle.

Map your regulatory obligations before writing a single requirement. Identify which compliance frameworks apply: SEC/FINRA, FCA, MiFID II, GDPR, and let these shape architecture decisions from the start.

This step is not optional. Skipping it guarantees rework.

List every custodian, market data provider, banking rail, and legacy system the platform must connect to.

This integration surface area is the primary driver of timeline and budget. Quantify it before estimating cost.

Map the advisor and client journeys separately. Advisors need workflow efficiency. Clients need transparency and self-service.

These two UX requirements often conflict. Resolving that tension is a design decision, not a development one.

Define the data model, WORM storage architecture, and audit trail schema before front-end design begins.

A compliance layer retrofitted after build completion inflates cost by an estimated 3–5×. Get it right here, or pay for it later.

Build custodian connectors, market data feed integrations, and identity/authentication infrastructure in parallel with the core application.

This work is typically on the critical path. Delays here delay everything else.

Develop portfolio management, financial planning, client portal, and compliance modules in prioritized sprints.

An MVP should deliver one full advisor workflow end-to-end, not a feature checklist scattered across all modules.

Validate all financial calculations against known benchmarks. Test edge cases with unusual portfolio structures.

Simulate high-load conditions. The platform must not fail during market volatility, which is exactly when advisors need it most.

Conduct a formal legal and compliance review before launch. For US-facing platforms, this includes legal sign-off on KYC/AML workflows, WORM storage validation, and SOC 2 Type II audit preparation. Do not skip this step to meet a launch date.

Launch using a phased rollout; pilot advisor team, then full firm, then multi-office. Cloud-native deployment (AWS, Azure, GCP) is the standard for scalability. Post-launch includes monitoring, security patching, and regulatory update cycles.

The commonly cited range “$40,000 to $600,000+” tells you almost nothing useful. What actually drives cost escalation are specific, quantifiable decisions your team makes before development starts.

| Cost Driver | Basic / MVP | Mid-Scale | Enterprise |

| Custodian Integrations | 1–2 (single custodian) | 2–4 custodians (+$30K–$60K per) | 5+ custodians (+$80K–$150K per) |

| Compliance Tier | Basic KYC/GDPR | SEC Rule 17a-4 + FINRA 3310 | Full SOC 2 Type II + multi-jurisdictional |

| Compliance Cost as % of Build | 8–12% | 15–20% | 20–25% (Emerline, 2026) |

| AI Feature Scope | Rule-based rebalancing | Predictive analytics | NLP personalization + GenAI copilot |

| Deployment Model | Cloud-hosted SaaS | Cloud + on-premise hybrid | Private cloud / multi-region |

| Legacy Migration | None | Partial data migration | Full legacy system decommission |

| Estimated Total Build Cost | $80K–$150K | $200K–$350K | $400K–$600K+ |

| Estimated Timeline | 6–9 months | 10–14 months | 15–24 months |

Sources: Emerline (2026), Fortune Business Insights (2026).

| Note: Costs reflect US-market standards. Offshore development teams may reduce total cost by 30–50% with appropriate oversight and quality controls. |

These are not trends to monitor from a distance. They are architectural decisions to make now.

The Forbes “72-Hour Rule” captures this precisely: AI can replicate any feature-level innovation within 72 hours of launch. Sustainable competitive advantage now lives in backend infrastructure, data quality, and proprietary client data, not in your chatbot interface.

63% of wealth management firms are increasing cloud usage (The Wealth Mosaic, 2026). The shift from monolithic suites to modular, interoperable platforms is accelerating.

An API-first architecture that connects best-of-breed tools is no longer a technical preference; it is a business model decision.

NLP engines that analyze 50+ data points per client interaction are enabling advisors to serve 2–3× more clients without reducing service quality.

Firms without this capability are already losing the HNWI segment.

Generative AI copilots now draft meeting notes, investment policy statements, and rebalancing orders within seconds. Early adopters are achieving higher client-to-advisor ratios without lowering service quality (Mordor Intelligence, 2026).

Firms building now for millennial and Gen Z inheritors must architect for different engagement preferences: mobile-first, real-time notification-driven, and deeply integrated with alternative investment access.

62% of single-family offices aim to move off spreadsheets for consolidated reporting by 2026 (Mordor Intelligence). They need a platform to move to.

The compliance tier decision is the most consequential budget lever. Moving from a basic KYC build to a full SOC 2 Type II + FINRA-compliant architecture typically adds $60,000–$120,000 to the total cost. For any firm serving US-regulated clients, this is not a negotiable line item.

Every firm hits the same five walls. Knowing where they are lets you engineer around them before they stall your project.

Challenge 1 — Legacy System Integration

Most established firms run on fragmented, aging infrastructure. Creating a unified data layer across these systems is architecturally complex.

It often represents 25–35% of the total project scope. Map every legacy integration point in the discovery phase, before budgeting begins.

Challenge 2 — Compliance Retrofitting

Compliance requirements identified after development is underway cost significantly more to address than those designed in from the start.

The only solution is compliance-first architecture (see the section above). A compliance review at the end of the build is not a substitute.

Challenge 3 — Custodian API Availability & Data Normalization

Each custodian returns data in different formats, on different latencies, with different API rate limits. Building a normalization layer that unifies this data is complex and time-consuming.

Budget for it explicitly and assign a dedicated integration engineer. This is not a task to distribute across the team.

Challenge 4 — Advisor Adoption & Change Management

Technical success does not guarantee adoption. Advisors will revert to familiar workflows if the new platform isn’t meaningfully faster for their most frequent tasks.

Include advisors in UX research from the start, not the UAT phase.

Challenge 5 — Cybersecurity at Financial-Grade Standards

Financial services firms experience 300× more cyberattacks than firms in other sectors (KnowBe4). Annual security protocol spending is increasing by 15% within wealth software development as a direct result.

SOC 2 Type II certification is not just a compliance checkbox; it is a client acquisition tool at the enterprise level.

The credibility gap in wealth management software development partnerships is not about technical capability. The gap is domain depth in financial services compliance, integration architecture, and regulated-market delivery.

Code Brew Labs has built fintech platforms that operate under real regulatory constraints, serve millions of users, and hold up when the compliance scrutiny comes.

Two things differentiate how Code Brew Labs builds for regulated financial markets:

First:

Compliance-first architecture from Day One, not as an afterthought. The data model, WORM storage architecture, and audit trail schema are defined before front-end design begins. This is why our builds don’t require expensive rework after delivery.

Second:

Integration architects who have built custodian-connected, audit-ready platforms across regulated financial markets. Your build starts with the hardest problems already solved.

Wealth management software development is the process of designing, building, and deploying a technology platform that enables financial advisors and institutions to manage client portfolios, automate compliance workflows, deliver financial planning, and give clients real-time access to their financial data.

Development cost ranges from approximately $80,000 for a compliance-grade MVP with a single custodian integration to $400,000–$600,000+ for a full enterprise platform with multi-custodian connectivity, SOC 2 Type II compliance, and AI-powered personalization.

A well-scoped MVP typically takes 6–9 months to build. A mid-scale platform with multiple custodian integrations and SEC/FINRA-compliant architecture typically takes 10–14 months. An enterprise platform with legacy migration, multi-region deployment, and AI infrastructure typically takes 15–24 months from discovery to launch.

For most established wealth management firms, the answer is neither; it’s hybrid. Build the core data aggregation layer and compliance architecture custom to retain control and ensure auditability. Procure best-of-breed modules for financial planning or client portal functionality. Full custom builds make sense when your advisory model or investment strategy is genuinely proprietary.

Essential integrations include: custodians (Schwab, Fidelity, Pershing, Orion), market data feeds (Bloomberg, Refinitiv, Morningstar), KYC/AML providers (Fenergo, Compliancely, NICE Actimize), open banking rails (Plaid, FDX API), and authentication protocols (OAuth 2.0, SAML). For broker-dealer platforms, FIX protocol integration for order routing is also required.

US-regulated platforms must address SEC Rule 17a-4 (WORM recordkeeping), FINRA Rule 3310 (AML program requirements), KYC/AML onboarding workflows, and SOC 2 Type II certification for data security. UK/EU platforms add MiFID II and GDPR. Multi-jurisdictional platforms must build data residency and consent management into the data model architecture from the start.

Priority AI features for 2026 include: portfolio rebalancing automation, NLP-driven hyper-personalized client proposals, predictive cash flow analysis, GenAI copilots for meeting notes and investment policy statements, and anomaly detection for compliance monitoring. All AI outputs must maintain an auditable log of inputs, outputs, and human overrides to meet regulatory requirements.

Contact Us

Contact UsTeam Up With Us Today For An Unforgettable Service Experience

Book Free Consultation

Book Free Consultation