Table of Content

Key Takeaways

- Mobile banking apps are now core infrastructure, with 70%+ of interactions happening on mobile.

- Compliance-first architecture is critical, with GDPR penalties reaching up to 4% of global revenue.

- The four-layer architecture (Frontend, Backend, Security, Cloud) drives scalability and resilience.

- Development costs range from $40K–$120K (MVP) to $500K+ (enterprise platforms).

- KYC onboarding delivers the highest ROI, reducing drop-offs by 20–30%.

- Build vs Buy decisions directly impact speed, cost, and long-term flexibility.

- Cloud-native microservices improve deployment speed by 30–50%.

Table of Content

The mobile app is no longer a channel for your bank.

It is your bank.

In 2026, customers open accounts, approve loans, dispute transactions, and move large sums without human interaction. The global neobanking market reached $210 billion in 2025 and is growing at a 49.3% CAGR(global neobanking market report). Banks that treat mobile as a front-end will lose to those that treat it as core infrastructure.

This guide is for decision-makers. It covers the architecture, compliance, cost models, and build vs buy strategies that determine whether your banking app scales, secures market access, and competes effectively. If you’re launching or re-platforming a product, this is what you need before engaging a development partner.

What Is Mobile Banking App Development — And Why the Definition Matters in 2026

Mobile banking application development is the end-to-end process of designing and deploying a financial app.

It enables users to access banking services like payments, onboarding, lending, and investments from a smartphone.

That definition sounds simple. The execution is not.

The visible layer (what users see) is only about 20% of the engineering effort.

The remaining 80% sits in backend systems: core banking integrations, fraud detection, KYC orchestration, and real-time ledger infrastructure.

What separates successful fintech apps from failed ones is not the feature list. It is the architecture decisions made in the first eight weeks of a project.

The categories of mobile banking apps being built and deployed today include:

- Retail banking apps (account management, bill payments, card controls)

- Neobank and challenger bank apps (digital-only, no branch dependency)

- Payment and digital wallet apps (P2P, QR, cross-border transfers)

- Investment and wealth management apps (robo-advisory, portfolio tracking)

- BNPL and credit apps (instant lending, installment management)

- Business banking apps (treasury, payroll, multi-entity management)

The Business Case — Why 2026 Is the Inflection Point

Three forces have converged to make 2026 the highest-stakes year in digital banking.

First, the channel shift is complete.

Mobile is now the primary channel for account openings, cross-selling, and card management.

For users under 45, branch banking is no longer the default.

Second, profitability is no longer a question.

Digital banks are proving they can scale—and generate real profits.

Revolut reported £1.1 billion in pretax profit in 2024, with revenue growing 72% year over year.

Nubank now serves over 110 million users.

The idea that digital banking cannot be profitable is no longer valid.

Third, competition has changed.

Banks are no longer competing only with other banks.

Amazon, Apple, and Google are all entering financial services.

In this environment, a poorly architected banking app isn’t just a disadvantage.

It’s a long-term risk.

For CTOs and founders, the question in 2026 is not whether to build a mobile banking app.

It’s whether to build one that can compete at the infrastructure level.

Core Architecture — The Four Layers Every Banking App Must Get Right

Every production-grade mobile banking app operates across four interdependent layers. Getting any one wrong creates technical debt that often requires a full rebuild.

Layer 1: Frontend and UX Architecture

Native development using Swift (iOS) and Kotlin (Android) offers the highest security, performance, and access to device features like biometrics and secure storage, but requires separate codebases.

Flutter (cross-platform) is the recommended 2026 approach for most fintech apps, enabling a single codebase with near-native performance and faster time-to-market.

Frontend approach:

- Native: Maximum performance and security

- Flutter: Faster development with near-native experience

- Hybrid: Not suitable for customer-facing banking apps

Layer 2: Backend and Microservices Architecture

Monolithic backends do not scale. Modern banking app backend architecture relies on microservices, which break the system into independent services for authentication, ledger management, payments, KYC, fraud detection, and notifications.

Each service scales independently, ensuring high availability during transaction spikes.

Recommended 2026 tech stack:

- Backend: Java (Spring Boot) for transactional integrity and compliance

- Database: Oracle (core ledger) + PostgreSQL (cloud-native services)

- API Layer: REST + GraphQL

- Event Streaming: Apache Kafka for real-time processing

Layer 3: Security Architecture

In mobile banking app security architecture, security is not a feature; it is the system itself.

Key threat vectors and controls:

- Man-in-the-middle: TLS 1.3, certificate pinning

- Session hijacking: JWT tokens, device fingerprinting

- Reverse engineering: code obfuscation, jailbreak detection

- Credential attacks: behavioral biometrics, adaptive MFA

- Insider threats: RBAC, audit logs

The OWASP MASVS standard defines the baseline, with Level 2 recommended for regulated apps. Real-time fraud detection can reduce losses by 30–50%.

Layer 4: Cloud Infrastructure

Cloud-native architecture is essential for scalability in mobile banking app development. AWS, Google Cloud, and Azure enable auto-scaling, global distribution, and rapid deployment.

Infrastructure must align with compliance:

- EU: GDPR data localization

- India: RBI data localization

- MENA: regional cloud requirements

AWS remains the default choice for most fintech teams due to its fintech-ready frameworks.

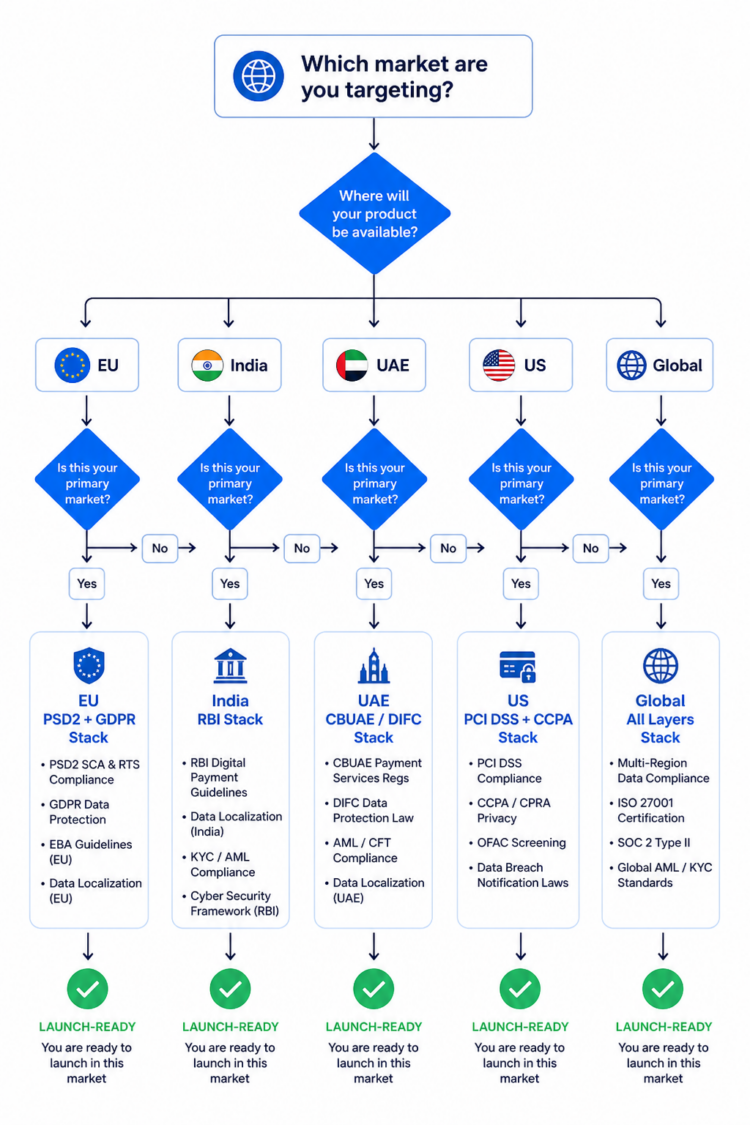

Banking App Compliance Requirements — The Framework That Determines Market Access

Compliance is not a legal checkbox appended to a completed product. It is a design constraint that must be embedded into the architecture from day one.

Teams that introduce compliance requirements after the development phase face one outcome: expensive redesigns and delayed launches. This is the single most common source of mobile banking project failure at the board level.

The regulatory framework your app must address depends on the market you are targeting. The following table covers the primary compliance requirements for the top global fintech markets:

GLOBAL COMPLIANCE REQUIREMENTS BY MARKET

| Regulation | Market | What It Governs | Penalty for Non-Compliance |

| PCI DSS | Global | Card data security and secure transmission | Fines + card network bans |

| GDPR | EU / EEA | User data handling and right to erasure | Up to 4% of global revenue |

| PSD2 | EU / EEA | Open banking and third-party API access | Market access revocation |

| RBI Guidelines | India | Data localization and payment processing | License revocation |

| AML / KYC | Global | Identity verification and fraud prevention | Criminal liability |

| PCI PA-DSS | Global | Payment application security | Certification withdrawal |

| CCPA | United States | Consumer data rights (California) | Per-violation civil fines |

| DIFC / ADGM | UAE | Financial services and FinTech sandbox rules | Operating license suspension |

Three compliance pillars require the deepest architectural integration:

1. KYC (Know Your Customer)

KYC is not just a compliance requirement—it is your primary growth funnel.

Poor onboarding flows can lead to drop-off rates of over 60%.

Well-optimized flows significantly improve conversion and reduce manual effort.

Modern KYC systems must support:

- Digital identity verification

- Liveness detection

- Document scanning

- PEP and sanctions screening

All of this needs to happen in a fast, seamless flow—ideally under three minutes for standard users.

2. AML (Anti-Money Laundering)

AML systems must operate in real time.

Basic rule-based systems are no longer enough.

Production-grade platforms combine rules with machine learning models.

These systems detect:

- Unusual transaction patterns

- Velocity anomalies

- Network-level suspicious activity

The goal is to identify risks early—before regulatory reporting becomes mandatory.

3. Open Banking APIs

Open banking is no longer optional in regulated markets.

Frameworks like PSD2 and RBI guidelines require secure third-party data access.

This directly impacts how your API layer is designed.

Key requirements include:

- OAuth 2.0-based authentication

- Rate limiting and API security controls

- User consent management systems

These cannot be retrofitted later.

They must be built into your architecture from the start.

Must-Have Banking App Features

Not all features are equal. Some are compliance requirements, some are revenue enablers, and some are retention drivers.

FEATURE PRIORITIZATION MATRIX

| Feature | Category | Business Function | MVP? | Phase |

| Biometric Authentication | Security | Trust, regulatory compliance | Yes | 1 |

| Digital KYC / eKYC | Compliance | Onboarding conversion | Yes | 1 |

| Account Dashboard | Core UX | Daily active use driver | Yes | 1 |

| Fund Transfers (P2P, IMPS) | Payments | Primary revenue enabler | Yes | 1 |

| Push Notifications | Engagement | Retention, fraud alerting | Yes | 1 |

| Card Management | Core Feature | Interchange revenue | Yes | 1 |

| Bill Payments | Core Feature | Stickiness, daily utility | Yes | 1 |

| Transaction History | Core UX | Compliance + user trust | Yes | 1 |

| AI Spending Insights | Differentiation | ARPU growth, retention | No | 2 |

| Cross-Border Payments | Expansion | Premium revenue | No | 2 |

| Open Banking Integration | Ecosystem | Market access (EU/UK) | No | 2 |

| Investment / Robo-Advisory | Revenue | Diversified income stream | No | 3 |

| BNPL / Credit | Revenue | High-margin lending income | No | 3 |

| Voice Banking | Engagement | Accessibility, differentiation | No | 3 |

The feature that most teams under-invest in relative to its business impact is the onboarding flow. Reducing onboarding time from an industry-average of 8-12 minutes to under 3 minutes can increase conversion by 20-30%.

Every week of engineering invested in an optimized, automated KYC flow delivers higher ROI than most Phase 2 features combined.

Build vs Buy vs White-Label — A Framework for the Right Decision

This is the decision that determines your time-to-market, your total cost of ownership, and the long-term flexibility of your product. Most guides skip it entirely. Here is the decision framework.

BUILD VS BUY VS WHITE-LABEL COMPARISON

| Dimension | Custom Build | White-Label Platform | BaaS Partnership |

| Time to Market | 9–18 months | 2–4 months | 1–3 months |

| Initial Cost | $150K – $500K+ | $30K – $150K | Low / Revenue Share |

| Customization | Full | Limited to Moderate | Low |

| Compliance Control | Full Ownership | Shared | Vendor-Dependent |

| IP Ownership | 100% Yours | None | None |

| Scalability | Unlimited (by design) | Platform-Constrained | Vendor-Constrained |

| Vendor Lock-in Risk | None | Moderate | High |

| Best For | Neobanks, Tier-1 Enterprise Banks | Regional Fintechs, Rapid Pilots | Embedded Finance, Non-Bank Products |

The decision rule:

If you are building a product where differentiation is the core of your business model, such as a neobank or financial super-app, a regulated digital bank — build custom. The long-term cost of vendor constraints exceeds the short-term cost of custom development.

If you need a regulated MVP in the market in under six months to validate commercial assumptions before raising a Series A, white-label accelerated by a development partner is the rational choice.

If you are a non-financial business adding embedded finance, such as a retailer adding BNPL, a gig platform adding early wage access — BaaS is the right model.

Do not let short-term cost concerns drive a build-vs-buy decision that will constrain your architecture for five years.

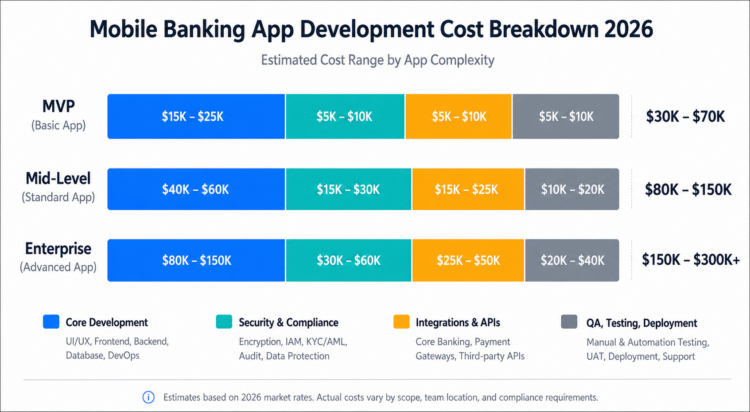

Cost to Build a Mobile Banking App in 2026

The cost range for mobile banking app development in 2026 spans $40,000 to $500,000+. That range reflects genuinely different products.

COST TIERS — MOBILE BANKING APP DEVELOPMENT 2026

| Tier | Cost Range (USD) | Estimated Timeline | What’s Included |

| MVP / Basic | $40,000 – $120,000 | 3–6 months | Core accounts, money transfers, basic KYC, standard authentication |

| Mid-Level Platform | $120,000 – $300,000 | 6–10 months | Full KYC, fraud detection, bill payments, card management, open banking APIs |

| Enterprise / Neobank | $300,000 – $500,000+ | 9–18 months | Custom core banking, AI-powered features, multi-market compliance, full DevSecOps |

Hidden cost drivers that inflate budgets, often discovered too late by clients:

Compliance infrastructure: Regulatory audit preparation, penetration testing, and PCI DSS Level 1 certification can add $40,000-$80,000 independent of feature scope.

Third-party integrations: Each integration, including payment gateways, KYC providers, and credit bureaus, fraud detection engines add 2–4 weeks of engineering time plus ongoing API licensing costs.

Total Cost of Ownership: Annual maintenance includes OS updates, security patches, compliance monitoring, infrastructure scaling — typically runs 20-30% of the initial build cost per year. A $200,000 build has a 5-year TCO of $400,000-$500,000.

Team geography: Development teams in North America and Western Europe charge $120-200/hour. Comparable teams in South Asia or Eastern Europe charge $35-80/hour, creating a 3-5x cost differential that materially affects budget without affecting quality when the right partner is selected.

McKinsey Banking Review confirms banks globally spend approximately $600 billion annually on technology, confirming that maintenance and operational IT represent the majority of total financial services technology spend.

The timeline framework below is built around avoiding both failure modes.

Phase 1 — Discovery and Compliance Scoping (Weeks 1-4)

Define product objectives, user personas, and regulatory scope. Map compliance requirements by target market before a single line of code is written. Conduct threat modeling and define security requirements.

Output: Technical specification, compliance matrix, API integration plan.

Phase 2 — UX/UI Design and Prototyping (Weeks 5-9)

Wireframe critical user journeys such as onboarding, payments, and card management. Prototype the KYC flow with drop-off optimization as the primary design metric. Validate prototypes with target users before development begins.

Output: High-fidelity prototypes, design system, accessibility audit.

Phase 3 — Development Sprint Cycles (Weeks 10-24+)

Backend microservices built before frontend begins. Security controls integrated into each sprint, not added post-build. API integrations built in parallel development tracks.

Output: Feature-complete application with integrated security layer.

Phase 4 — QA, Security Testing, and Compliance Audit (Weeks 24-28+)

Penetration testing against OWASP MASVS Level 2 standard. Load testing for peak transaction volumes. Regulatory compliance audit and documentation preparation.

Output: Security audit report, compliance documentation, launch-ready build.

Phase 5 — Deployment and Post-Launch Optimization (Weeks 28+)

Staged rollout from beta to regional to full deployment. Real-time monitoring, fraud detection calibration, performance tuning. Ongoing monthly security patches and quarterly feature updates.

Output: Live app, monitored infrastructure, optimized performance, and continuous update pipeline.

Case Study — DuPay: Scaling Payroll & Payments Infrastructure

Problem:

DuPay needed a secure, scalable platform to enable cashless payroll and digital payments for unbanked workers, while handling high transaction volumes and meeting strict compliance requirements. As the platform grew, challenges emerged around data scalability, real-time visibility, and secure access control.

Solution:

Code Brew Labs built a cloud-native, microservices-based architecture designed for fintech scale:

- Modular services for payroll, transactions, and KYC

- Real-time data pipelines for high-volume processing

- Secure backend with role-based access and audit trails

- Integrated analytics for operational and compliance visibility

Results:

- Processed 5M+ records per month with stable performance

- Enabled near real-time data visibility for decision-making

- Strengthened security and compliance readiness

- Reduced dependency on engineering for reporting and insights

Key Insight: A compliance-first, scalable architecture allowed DuPay to grow efficiently without rebuilding its core systems.

Building a fintech platform? Start with the right architecture

Frequently Asked Questions

How much does mobile banking app development cost in 2026?

Mobile banking app development costs range from $40,000 for a basic MVP to $500,000 or more for an enterprise-grade neobank platform. The actual cost is determined by feature scope, security requirements, compliance infrastructure, third-party integrations, and team geography. Most production-grade, compliant banking apps for startup and mid-market clients fall between $120,000 and $300,000. Annual maintenance typically adds 20-30% of the initial build cost per year.

How long does it take to build a mobile banking app?

A basic MVP with core banking features takes 3-6 months. A full-featured platform with compliance infrastructure, fraud detection, and open banking integrations takes 6-12 months. Enterprise-grade builds with custom core banking and multi-market compliance take 12-18 months. Phased development, where you launch an MVP first and iterate, is the recommended approach for startups targeting a funding milestone.

What compliance requirements apply to mobile banking apps?

Compliance requirements depend on your target market. PCI DSS applies globally to any app handling card data. GDPR applies to all EU/EEA users. PSD2 governs open banking in Europe. RBI guidelines apply to India-facing financial products. KYC and AML obligations apply in virtually every regulated market. Compliance must be architected from day one and not added after development is complete.

Is Flutter secure enough for a mobile banking app?

Yes. Flutter compiles to native code, providing security and performance equivalent to native iOS or Android development for most banking use cases. It also enables faster time-to-market with a single codebase. It is the recommended cross-platform framework for fintech applications in 2026.

Can fintech startups build banking apps without a banking license?

Yes. Options include partnering with a sponsor bank, obtaining an Electronic Money Institution (EMI) license, using a Banking-as-a-Service provider, or applying for a regulatory sandbox license such as the DFSA sandbox in Dubai or the FCA sandbox in the UK. A fintech compliance attorney should be engaged before selecting the regulatory pathway.

What is the most important feature in a mobile banking app?

From a business perspective: the onboarding flow. Onboarding is the conversion funnel for every downstream feature. Reducing onboarding time to under three minutes can increase completion rates by 20-30%. From a trust perspective: security and fraud detection, because no retention strategy survives a high-profile security incident.

What is the difference between a neobank and a traditional mobile banking app?

A traditional mobile banking app is a digital channel for an existing institution where users have an underlying account at a bank with branch infrastructure. A neobank is a digital-only institution that exists entirely within the mobile experience with no branches and no legacy infrastructure, and an architecture designed from the ground up for mobile. The engineering implications are significant: neobanks require fully custom core banking infrastructure or deep BaaS integration.

Conclusion

Mobile banking application development in 2026 is not a software project. It is an infrastructure decision with a 5-10 year compounding impact on your organization’s competitive position, regulatory standing, and revenue potential.

The decisions made in the first eight weeks — architecture patterns, compliance scope, tech stack selection, build-vs-buy framework — determine whether your app scales to 50 million users or gets rebuilt two years after launch.

Code Brew Labs has delivered mobile banking and fintech applications across the UAE, South Asia, Southeast Asia, and MENA for over a decade. Our engineering teams bring compliance-first architecture, security-by-design development practices, and the product strategy experience to take a mobile banking concept from whiteboard to regulated, production-grade launch.

If you are planning a mobile banking product, a digital lending platform, or a fintech application for a regulated market, start with a conversation.

Ready to Build a Mobile Banking App?

Let's Convert Your Business Idea Into Success!

Free Consultation from Top Industry Experts

Let’s Build Your Dream App!

Share article on :

Ready To Fuel Your Vision With AI-Powered Innovation?

Level- 18, Dubai World Trade Centre Tower, Sheikh Rashid Tower, Sheikh Zayed Rd, Dubai, UAE

business@code-brew.com +971-55-645-7972

Plot no I - 36, Sector 83 Alpha, Mohali SAS Nagar 140308

business@code-brew.com +91-771-976-8427

Av. Miguel Hidalgo y Costilla 1995, Arcos Vallarta, 44600 Guadalajara, Mexico

business@code-brew.com +1(213)2614953

4231 Balboa Ave #512 San Diego, CA 92117 United States

business@code-brew.com +1(213)2614953

2nd floor, College House, 17 King Edwards Rd, London HA4 7AE, UK

business@code-brew.com +44 (20) 82644493

Partner With Experts Who Leverage AI & Tech To Transform Ideas Into Market-Leading Solutions.

Wait! Looking for Right Technology Partner For Your Business Growth?

It's Time To Convert Your Business Idea Into Success!

Get Free Consultation From Top Industry Experts:

I would like to keep it to myself