Key Takeaways

Table of Content

Fintech app development in the UAE is the process of building secure and compliant financial applications such as digital banking apps, payment wallets, lending platforms, and investment solutions while adhering to regulations set by the CBUAE, DIFC, and ADGM.

Businesses often partner with a fintech app development company in the UAE to build scalable solutions across Dubai and Abu Dhabi, where demand for digital financial services is growing rapidly. The UAE fintech sector continues to expand as part of the country’s broader digital economy, which is projected to reach $140B by 2031, driven by mobile banking, cashless payments, and financial innovation initiatives.

The cost of fintech solutions in the UAE depends on features, integrations, security requirements, and compliance complexity, making proper planning essential before development begins.

This guide explains fintech app development in the UAE, including cost, features, licensing requirements, UAE PASS integration, banking APIs, and key fintech trends shaping Dubai and Abu Dhabi.

Fintech app development in the UAE is the process of building secure, compliant financial applications that support payments, digital banking, lending, and investment services while meeting regulations set by CBUAE, DIFC, and ADGM.

Most fintech apps in the UAE fail not because of poor design, but because they underestimate compliance complexity and banking integrations.

Dubai has emerged as a regional fintech hub through DIFC, ADGM, and regulatory sandboxes that enable innovation while maintaining financial stability. This rapid ecosystem growth is supported by collaboration with best app development companies, helping startups and enterprises build scalable fintech platforms aligned with UAE market demand.

Cashless payments, app-based banking, and real-time transfers are becoming the default. Traditional financial services are being replaced by mobile-driven ecosystems where speed, transparency, and convenience define user expectations.

More importantly, the UAE government isn’t just supporting fintech — it’s actively accelerating it through structured regulations and investment-friendly policies.

Key trends shaping the market include:

| Metric | Value |

| UAE Fintech Market Size | Rapidly growing multi-billion sector |

| Digital Payments Adoption | Increasing across Dubai & Abu Dhabi |

| Government Support | DIFC, ADGM, CBUAE initiatives |

| Key Growth Driver | Cashless economy transition |

Yes, fintech in the UAE is strictly regulated by authorities such as the Central Bank of the UAE (CBUAE), DIFC, and ADGM. Apps must comply with AML, KYC, and data protection laws to operate legally.

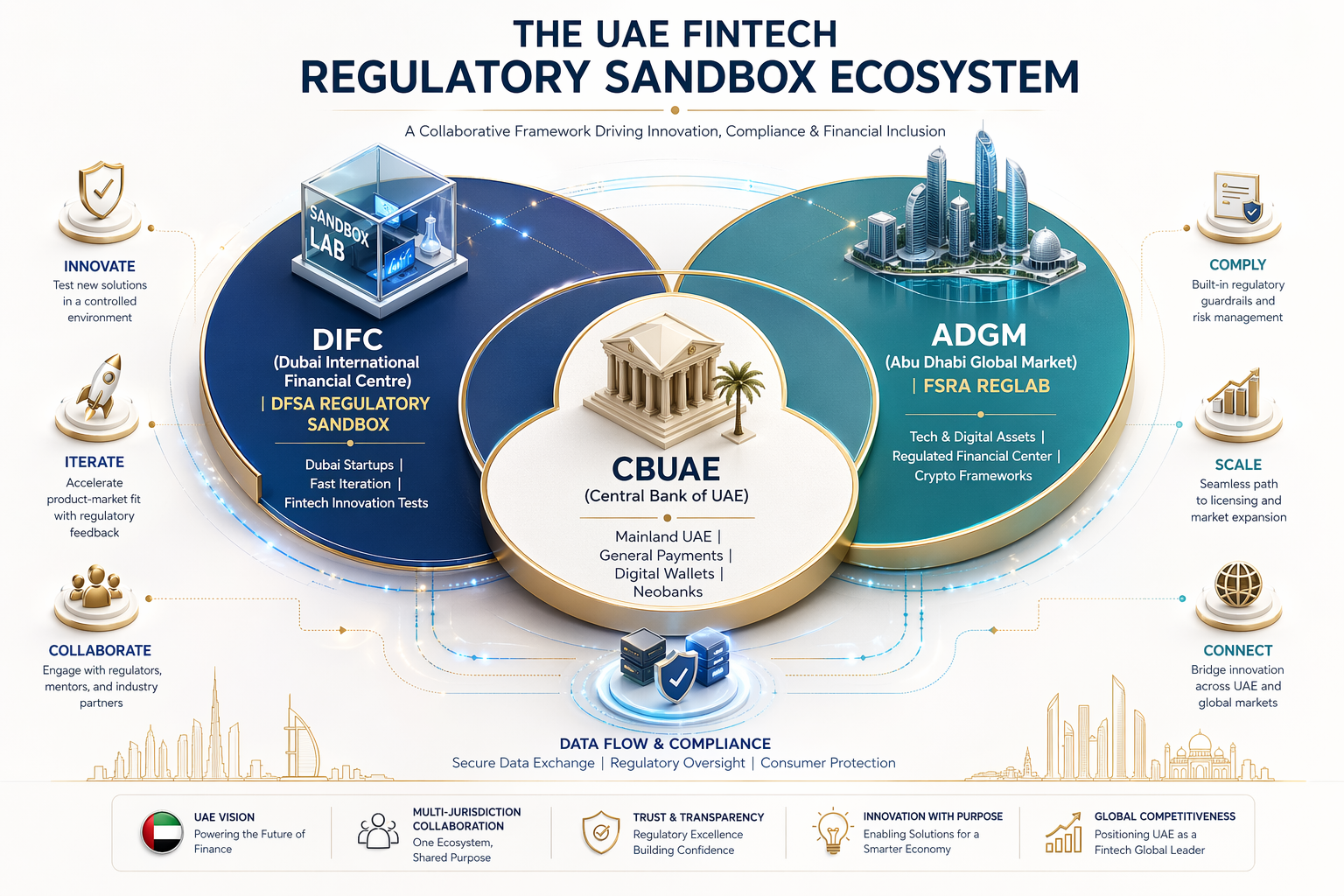

UAE fintech regulatory ecosystem showing jurisdiction layers across CBUAE (mainland), DIFC (DFSA sandbox), and ADGM (FSRA RegLab) for fintech compliance and innovation

In fintech app development company UAE, everything starts with regulation. UAE fintech regulations 2026 continue to evolve, requiring apps to comply with frameworks set by CBUAE, DIFC, and ADGM.

A core requirement is compliance with AML (Anti-Money Laundering) and KYC (Know Your Customer) regulations, which are enforced by the Central Bank of the UAE (CBUAE).

Applications must integrate identity verification, transaction monitoring, and risk assessment systems to ensure transparency and prevent fraud.

Data protection is equally critical. Platforms must follow UAE data privacy laws, ensuring secure handling of financial and personal data through encryption, access control, and local data storage requirements.

Depending on the business model, licensing may include:

Within DIFC and ADGM, additional frameworks such as DFSA guidelines govern fintech operations in regulated sandbox environments.

| Regulation | Scope | Applies To | Key Role |

| CBUAE | Banking & payments | All fintech apps | Licensing & oversight |

| DIFC | Financial sandbox | Dubai startups | Innovation support |

| ADGM | Financial ecosystem | Abu Dhabi fintech | Investment & crypto regulation |

| AML | Fraud prevention | All platforms | Risk monitoring |

| KYC | Identity verification | All users | User authentication |

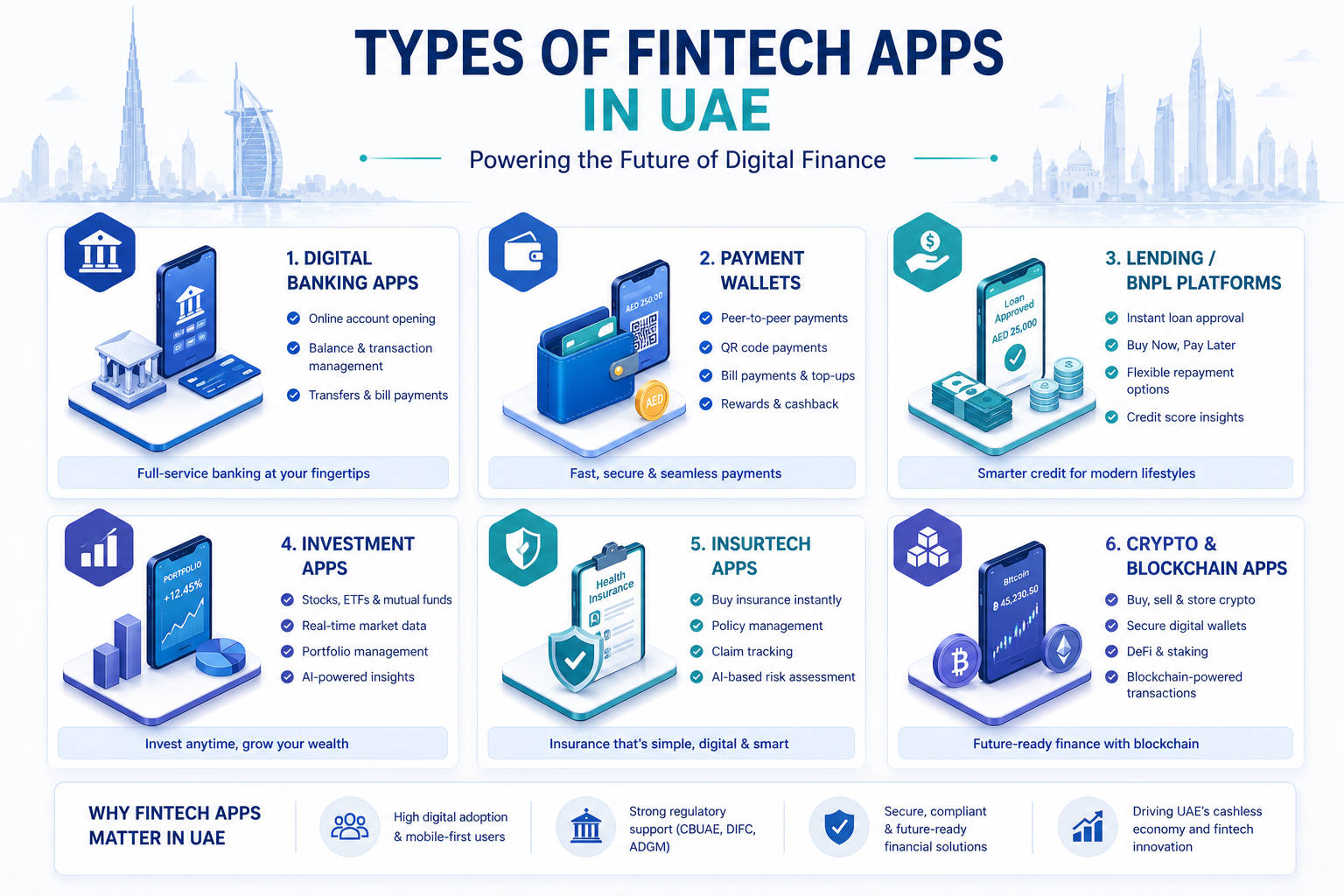

Digital financial solutions in the UAE span multiple app categories, each addressing specific financial use cases within the digital economy.

Overview of major fintech app categories in the UAE, covering banking, payments, lending, investment, insurance, and blockchain-based platforms

Digital banking apps are cloud-based platforms that allow users to open accounts, manage finances, and access banking services without physical branches. They offer features such as savings accounts, transfers, debit cards, and transaction tracking within a fully digital experience.

In the UAE, neobanks are gaining traction due to high smartphone usage and demand for seamless financial services. Common features include instant onboarding, virtual cards, spending insights, and real-time alerts. Advanced platforms also use AI for personalized financial recommendations.

For businesses looking to scale in this space, build fintech payment wallet apps play a key role in delivering secure and scalable digital banking experiences.

Payment wallets are among the most widely adopted fintech solutions in the UAE, driven by the shift toward a cashless economy.

These apps enable users to store funds digitally and perform peer-to-peer transfers, merchant payments, bill payments, and QR-based transactions instantly.

Modern wallets function as complete financial ecosystems by integrating with banks, card networks, and payment gateways. Features like split payments, recurring billing, and rewards programs are becoming standard.

Lending and BNPL apps are transforming access to credit by offering faster, more transparent borrowing options.

These platforms use real-time data analysis, behavioral scoring, and automated risk models to assess eligibility. BNPL allows users to split payments into installments, while lending apps offer personal loans, micro-credit, and SME financing.

AI-driven credit scoring and fraud detection play a critical role in minimizing risk and improving approval speed.

Investment fintech apps are designed to give retail users direct access to financial markets, enabling investments in stocks, ETFs, mutual funds, and other assets depending on regulatory permissions.

In the UAE, growing financial awareness is driving adoption of these platforms. Key features include portfolio tracking, real-time data, automated investing, and AI-based insights.

Advanced platforms also offer robo-advisory services that recommend portfolio strategies based on user goals and risk tolerance.

Insurance technology apps are modernizing the insurance experience by simplifying policy purchase, claims processing, and renewals.

Users can compare policies, purchase coverage instantly, and submit claims digitally. AI is increasingly used to automate claim validation and detect fraud.

These platforms are particularly relevant in health, motor, and travel insurance segments in the UAE.

Crypto applications in the UAE are emerging within regulated frameworks, enabling secure digital asset transactions.

These apps allow users to buy, sell, store, and transfer digital assets securely.

Beyond trading, blockchain is also being used for cross-border payments, smart contracts, and asset tokenization. The UAE’s structured regulatory approach has made it one of the more stable regions for blockchain-based fintech innovation.

Security, custody solutions, and compliance monitoring are critical components of these platforms.

| Fintech Type | Primary Use Case | Target Users | Complexity | Development Time | Estimated Cost |

| Digital Banking | Full banking | Retail, SMEs | High | 6–12 months | High |

| Payment Wallets | Payments | Consumers | Medium | 3–6 months | Medium |

| BNPL / Lending | Credit | Shoppers, SMEs | Medium–High | 4–8 months | Medium–High |

| Investment Apps | Trading | Investors | High | 6–10 months | High |

| InsurTech | Insurance | Individuals | Medium | 4–7 months | Medium |

| Crypto Apps | Digital assets | Traders | High | 6–12 months | High |

In fintech app development in UAE, success is not defined only by features — it is defined by how deeply an app integrates into the local financial ecosystem. Without these integrations, even advanced fintech products fail to achieve real adoption.

For a broader understanding of how fintech systems scale across regional banking ecosystems, businesses can explore this detailed Middle East fintech development guide.

Fintech apps in the UAE require integration with UAE PASS for identity verification, banking APIs (Emirates NBD, FAB, ADCB), and payment gateways like Network International and Checkout.com to enable secure and real-time financial operations.

UAE PASS acts as the national digital identity layer. It allows users to verify themselves instantly using government-backed credentials.

Instead of:

Fintech apps can enable:

This directly improves conversion rates and compliance accuracy.

For technical integration details (API endpoints, deep linking, and error handling), visit the official UAE PASS Mobile Application Integration Guide.

Modern fintech apps in the UAE must connect directly with banking systems to remain functional and competitive.

Key integrations involve:

These integrations enable:

Without direct banking connectivity, even well-designed apps feel incomplete and struggle in real-world usage.

| System | Purpose |

| UAE PASS | Digital identity & KYC |

| Emirates NBD / FAB APIs | Banking connectivity |

| Network International | Payment processing |

| Checkout.com | Global payments |

Payment systems form the backbone of any fintech ecosystem.

UAE fintech apps typically integrate with:

Core capabilities cover:

This is what actually lets the app handle both everyday users and high-volume business transactions without breaking

Fintech apps in the UAE are not standalone digital products — they are extensions of regulated financial infrastructure.

Without proper integration:

With full integration:

Fintech app development in the UAE requires a balance of security, compliance, and seamless user experience.

What features are required in a fintech app in the UAE?

Key features of a fintech app in the UAE include:

Fintech apps in the UAE are expected to deliver bank-grade security, real-time performance, and seamless user experience to meet modern digital banking standards.

To meet this expectation, feature design must balance security, usability, and regulatory compliance from the ground up.

Layered architecture of key fintech app features, including user interface, payments, security systems, and compliance infrastructure

At this point, the question is no longer “what should the app do?” but “how seamless can the experience actually feel?”

At the core of every fintech application is a strong authentication system. This typically includes biometric login (Face ID / fingerprint), OTP verification, and multi-factor authentication.

Advanced systems also implement session security, device binding, and risk-based login detection to prevent unauthorized access in real time.

User onboarding is one of the most critical stages in fintech adoption.

Modern fintech apps typically offer:

The goal is simple: reduce onboarding time from days to minutes while maintaining compliance accuracy.

At the end of the day, users judge the entire product based on how smoothly transactions work.

Most successful fintech apps get these basics right before anything else:

The system must support real-time transaction tracking, confirmations, and failure handling without delays.

Security is not static in fintech — it is continuous.

AI models are increasingly used to:

This ensures proactive protection instead of reactive response.

Users expect visibility into their financial behavior.

A strong fintech app provides:

This transforms the app from a transaction tool into a financial management system.

Given the UAE’s global population, fintech apps must support multiple currencies and languages.

Key capabilities include:

This ensures accessibility for both local users and expatriates.

Behind every fintech app is a control system for operations and compliance teams.

Key capabilities include:

This layer ensures transparency, governance, and audit readiness.

Building a fintech app in the UAE isn’t like building a regular app. You’re dealing with real money, real risk, and strict regulations—so the tech stack has to be rock-solid from day one. Unlike standard mobile apps, fintech systems operate under strict performance, compliance, and security expectations.

The tech stack is therefore designed around three priorities: speed, security, and regulatory readiness.

Multi-layer fintech app architecture for UAE including frontend, secure APIs, UAE PASS integration, AI fraud detection, and cloud infrastructure.

The frontend defines how users interact with the financial system. It must be fast, intuitive, and highly responsive.

Common choices include:

These frameworks ensure consistent performance across devices while maintaining smooth transaction flows.

The backend is where all financial logic is processed. It handles transactions, authentication, APIs, and integrations with banking systems.

Typical technologies include:

This is what keeps the system reliable as transaction volume grows.

Fintech apps handle sensitive and high-volume data, so database design is critical.

Common systems include:

These systems ensure data integrity, consistency, and fast retrieval.

Fintech apps in the UAE must be cloud-ready with regional compliance support.

Preferred platforms:

Cloud infrastructure enables:

Security is the most critical component of fintech technology.

Core implementations include:

Every transaction is designed to be secure, traceable, and tamper-proof.

Fintech apps must connect with external ecosystems to function effectively.

Key integrations include:

This layer ensures real-world usability and regulatory alignment within the UAE financial ecosystem.

The fintech app development process includes:

Businesses looking to build fintech app Dubai solutions must follow a structured, compliance-driven development process.

Fintech app development in the UAE follows a structured, compliance-driven process. Unlike standard app development, every stage must align with financial regulations, security requirements, and integration standards used by banks and payment systems.

The goal isn’t just to build an app — it’s to build something that can actually operate as a financial product. For a deeper breakdown of each stage, businesses can refer to this detailed fintech development guide covering architecture, features, and scalability.

This is where the foundation is defined.

Teams identify:

A clear product scope is critical because fintech complexity increases rapidly with each added feature.

Fintech UX is different from normal app design. It must feel simple while handling complex financial flows.

Design focuses on:

Every screen is designed to reduce user hesitation and improve financial confidence.

The MVP stage focuses on building the core financial engine.

Core features include:

The MVP is designed to validate functionality before scaling into full financial ecosystems.

At this stage, the app connects with external financial systems.

Key integrations include:

This step transforms the product from a standalone app into a connected financial platform.

Fintech apps undergo rigorous testing before launch.

Key checks include:

Security is not a final step — it is continuously validated throughout development.

Once approved, the application is deployed on secure cloud infrastructure.

Key components include:

Deployment ensures the system is stable under real financial traffic.

After launch, fintech apps require constant optimization.

Ongoing improvements involve:

Fintech is not a one-time build — it is an evolving system.

Whether you’re a startup or enterprise, choosing the right approach to build fintech app Dubai platforms is key to long-term success.

What is the cost of fintech app development in the UAE?

The cost of fintech app development in UAE typically ranges from $25,000 to $500,000+, depending on complexity, compliance requirements, and integrations.

The cost of fintech app development varies significantly based on app complexity, compliance requirements, and the depth of financial integrations. Unlike standard mobile apps, fintech platforms require advanced security layers, regulatory alignment, and real-time transaction infrastructure, which directly impacts development cost.

In general, fintech costs are driven more by compliance, security, and integrations than just design or frontend development.

A basic fintech MVP typically includes user onboarding, simple wallet functionality, basic payments, and authentication systems.

This stage is used to validate the product idea in the market.

Typical characteristics:

This is the most common category for startups scaling in the UAE market.

It usually covers:

At this level, the app becomes a functional financial product, not just a prototype.

Enterprise fintech systems are designed for banks, large financial institutions, or regulated digital financial services.

Core systems include:

This category represents full-scale digital financial infrastructure.

| App Type | Complexity Level | Estimated Cost Range | Development Timeline | Key Components |

| MVP Fintech App | Low | $25,000 – $60,000 | 10–14 weeks | Basic wallet, login, simple payments |

| Mid-Level Fintech App | Medium | $60,000 – $150,000 | 4–8 months | KYC, payments, dashboards, APIs |

| Enterprise Fintech Platform | High | $150,000 – $500,000+ | 6–12 months | Banking integration, AI fraud detection, compliance systems |

Several factors determine the final development cost:

Systems designed for high transaction volumes require enterprise-grade infrastructure.

How long does it take to develop a fintech app in the UAE?

Fintech app development in the UAE usually takes 10 weeks to 12 months depending on complexity.

Timelines for UAE fintech app development depend on product complexity, regulatory requirements, and the number of system integrations involved. Unlike standard applications, fintech platforms go through extended validation cycles due to compliance, security, and banking connectivity requirements.

The MVP phase focuses on building a functional core product.

Core features include:

The goal is to launch quickly, validate user behavior, and gather feedback.

At this stage, the product evolves into a complete financial application.

This phase typically covers:

This is where the app becomes market-ready.

Enterprise-level fintech platforms require more time due to complexity.

Core systems include:

Fintech app development timelines in the UAE depend on compliance requirements, integrations, and overall system complexity.

Key factors include:

Fintech applications in the UAE are not just digital financial tools — they are revenue-driven ecosystems designed to generate consistent income from transactions, services, and financial interactions.

One of the most common monetization models is charging a small fee per transaction.

This includes:

Many fintech apps adopt subscription-based pricing.

Examples include:

Lending platforms generate revenue through structured financial services.

This includes:

Fintech platforms collaborate with financial partners.

This includes:

Advanced fintech apps expand monetization through additional tools.

These include:

Building a fintech application in the UAE is not just a technical exercise—it is a regulated financial engineering problem. Fintech app development in the UAE requires balancing compliance, security, and real-time financial performance from day one.

The opportunity is huge, but execution is where most fintech products struggle. While the market opportunity is strong, execution comes with multiple layers of complexity across compliance, security, and system integration. Understanding these challenges early is critical to building a scalable and trusted financial product.

Fintech applications must comply with multiple regulatory bodies such as the Central Bank of the UAE (CBUAE), AML frameworks, and data protection laws. In addition, DIFC and ADGM introduce their own financial governance structures.

The real challenge is not just meeting compliance requirements at launch, but continuously adapting to regulatory updates as policies evolve over time.

Financial platforms are high-value targets for cyber threats due to the sensitive nature of user and transaction data.

Common risks involve:

To address this, fintech systems require layered security architecture, real-time monitoring, and AI-driven fraud detection to proactively identify threats.

One of the biggest technical hurdles is connecting modern fintech apps with traditional banking infrastructure. Many banks still operate on legacy systems, which creates friction in integration.

Typical challenges are:

This makes integration strategy a critical part of fintech architecture planning.

In financial services, trust plays a defining role in adoption. Even well-built applications can struggle if users are not confident in their security and reliability.

Key concerns are:

Building trust requires transparent communication, intuitive UX, and consistently reliable performance.

Fintech applications must strike a balance between simplicity and strict regulatory requirements.

For example:

The goal is to create experiences that feel effortless to users while maintaining full compliance behind the scenes.

Fintech app development in the UAE involves challenges such as regulatory compliance (CBUAE, AML, KYC), secure banking integrations, fraud risk management, and balancing user experience with strict financial regulations. Overcoming these requires a compliance-first architecture and strong technical execution.

Despite these challenges, the UAE remains one of the most favorable environments globally for launching and scaling fintech products.

The UAE has emerged as one of the most attractive global hubs for fintech innovation, making fintech app development in the UAE highly scalable and future-ready. Its combination of strong infrastructure, progressive regulation, and digital-first consumers creates an ideal environment for financial technology growth.

The UAE has one of the highest smartphone penetration rates globally, with users actively embracing digital banking, wallets, and cashless payments.

This shift results in:

Consumers across Dubai, Abu Dhabi, and Sharjah already expect instant, app-based financial services.

The country offers a mature and highly regulated banking ecosystem supported by global and regional institutions.

Core strengths are:

This allows fintech platforms to build on top of existing systems instead of replacing them entirely.

The UAE government actively promotes fintech innovation through structured strategies and regulatory support.

Key initiatives involve:

This creates a balanced environment where innovation can grow without compromising financial stability.

Dubai and Abu Dhabi act as financial gateways connecting Europe, Asia, and Africa. Dubai International Financial Centre (DIFC) has become a leading fintech hub driving innovation and investment in financial services.

This enables fintech applications to:

The fintech ecosystem is supported by strong venture capital activity, accelerators, and financial free zones such as DIFC and ADGM.

This leads to:

The future of fintech app development in the UAE is moving beyond simple digital payments toward intelligent, automated, and interconnected financial ecosystems. Innovation is being driven by AI, real-time data systems, and regulatory-ready infrastructure.

Modern fintech platforms are also evolving with AI-powered fintech app development solutions to improve fraud detection and personalization.

Artificial intelligence is becoming a core layer in modern fintech platforms.

It enables:

This shift is pushing fintech toward hyper-personalized financial services.

Blockchain is evolving into a practical financial infrastructure layer.

Applications include:

The UAE’s regulatory clarity is accelerating real-world adoption.

Delayed financial processing is quickly becoming obsolete.

Future systems focus on:

This is redefining user expectations for speed and accessibility.

Financial services are increasingly integrated into non-financial platforms.

Examples include:

Finance is becoming invisible yet always accessible.

Dubai and Abu Dhabi are evolving toward fully connected digital economies.

This includes:

To understand how fintech app development works in real conditions, consider a typical UAE-based financial platform built from concept to scale.

A financial services company aimed to launch a digital wallet and lending platform for UAE users, offering instant financial access through a mobile-first experience.

However, they faced several challenges:

The system struggled to scale for growing transaction volumes.

The solution focused on building a fully digital fintech ecosystem with automation and compliance at its core.

Key components included:

Development was executed in phases. An MVP was launched first to validate user adoption, followed by deeper integrations and advanced features such as analytics and fraud detection.

After deployment, the platform achieved:

The system evolved from a basic wallet into a full-scale financial platform, demonstrating how fintech app development in the UAE can deliver scalable, compliant, and high-performance solutions.

What is fintech app development in the UAE?

Fintech app development in the UAE is the process of building secure, compliant financial applications that support payments, banking, lending, and investment services while aligning with regulations set by CBUAE, DIFC, and ADGM.

How much does fintech app development cost in the UAE?

The cost of fintech app development in the UAE depends on app complexity, security requirements, and system integrations. A basic fintech MVP with wallet and onboarding features requires lower investment, while mid-level apps include payment gateways, KYC, and dashboards. Enterprise fintech platforms involve banking integrations, advanced security, and compliance systems, making them significantly more expensive.

How long does it take to build a fintech app in the UAE?

Fintech app development timelines in the UAE vary based on scope and regulatory requirements. A basic MVP typically takes 10–14 weeks. A full fintech platform with integrations and compliance systems can take 4–8 months, while enterprise-grade financial systems may require 6–12 months depending on complexity and approvals.

Is fintech regulated in the UAE?

Yes, fintech in the UAE is strictly regulated. Financial applications must comply with the Central Bank of the UAE (CBUAE), as well as frameworks under DIFC and ADGM. Regulations include AML (Anti-Money Laundering), KYC (Know Your Customer), and data protection laws.

What is required to launch a fintech app in Dubai?

To launch a fintech app in Dubai, businesses need a clear product model, compliance alignment with UAE regulations, secure cloud infrastructure, banking or payment integrations, and identity verification systems. Depending on the service, regulatory approvals and licensing may also be required.

How do fintech apps integrate with UAE banks and payment systems?

Fintech apps in the UAE integrate with banks and payment processors using secure APIs. These integrations enable account access, transaction processing, and real-time payments while maintaining compliance with financial security standards.

Do fintech apps support UAE PASS or digital identity systems?

Yes, many fintech applications integrate UAE PASS to enable secure, government-backed digital identity verification. This reduces manual onboarding time, improves user experience, and ensures compliance with KYC requirements.

Are fintech apps in the UAE using AI technologies?

Yes, AI is widely used in fintech app development in the UAE. It supports fraud detection, credit scoring, user behavior analysis, and personalized financial insights, helping improve both security and user experience.

Why is the UAE a strong market for fintech startups?

The UAE offers high digital adoption, strong financial infrastructure, and government-backed innovation programs. Financial hubs like DIFC and ADGM, along with a growing cashless economy, make it one of the most attractive markets for fintech app development.

Building a fintech app in the UAE requires more than development—it requires compliance-ready engineering, secure architecture, and scalable financial systems aligned with CBUAE, DIFC, and ADGM regulations.

Code Brew Labs is an AI and app development company with 13+ years of experience building digital products and enterprise-grade fintech systems across global markets.

We help startups and enterprises design and scale financial platforms that are secure, compliant, and built for real transaction load.

Our expertise includes:

Whether you are launching a digital wallet, lending platform, or investment app, we focus on building systems that are not just functional—but ready for real users, real transactions, and real compliance environments.

If you are planning fintech app development in the UAE, we can help you move from idea to a scalable, regulation-ready product.

Contact Us

Contact UsTeam Up With Us Today For An Unforgettable Service Experience

Book Free Consultation

Book Free Consultation