The on-demand world is determined to break open all traditional ways of doing business, sparing no industry in its wake. While the world of Fintech was already ablaze with the sheer development it is undergoing at the moment (finance + technology at its best), another bad mashup term is doing the rounds – InsurTech. In this article, we’ll look at a few examples of InsurTech disrupting existing models.

Table of Content

I don’t think we need to explain the roots of this word, but yes, insurance is now being redefined by start-ups that want to cater to the demands of the millennial generation. The bottom line is, that millennials want more choice, more flexibility, and tons of time-saving efficient methodology as far as most things go, and their insurance is no exception. Also, when we do discuss insurance with the average millennial, it’s not the most interesting, or even ponder-worthy conversation – so why talk about it now?

Well, there’s a problem. You see, while many on-demand ventures may seem petty and niche-oriented, insurance is a definitive problem. Remember, the on-demand economy’s original spirit is to break apart traditional business models because they are stagnant in nature. If those methods worked fine, then nobody would mind, but that doesn’t seem to be the case – take the taxi-sharing world, the world of hoteliers, and what have you.

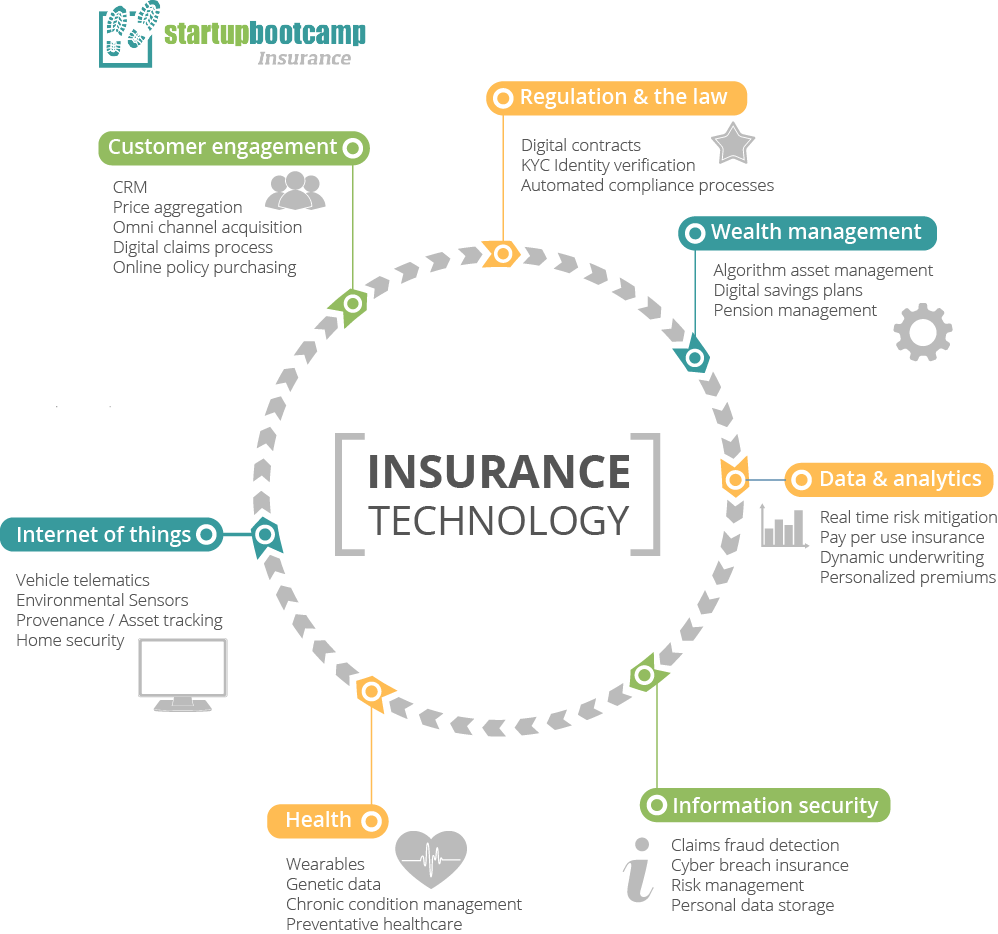

In addition the insurance industry is poised to change with the help of artificial intelligence, new payment systems, drones and blockchain technology.

First off, the whole concept of insurance has a shady, black box-like connotation.

Meaning that there’s simply not enough transparency when it comes to people actually knowing what their insurance grants them in the first place, and most companies seem to prefer keeping it that way. Alternatively, the terminology or the attempts to educate the insurer are often drab and seem far-fetched.

Another problem is the kind of insurance people purchase, and these are often not all that consumer centric. Many people insure assets that they might never see, ignoring the stuff they might need insurance for, and insure things at a time they might not need the insurance for.

But all of these concerns are tame as compared to the process of extracting insurance. Remember those famed, shady insurance companies and their lawsuits? They haven’t really gone anywhere, and the reason why they have such a connotation is that companies are highly reluctant to let go of their money – and rightly so, when it comes to fraud and other such. So, there need to be smarter, faster and more streamlined ways of verifying an insurance claim in the first place, and the transfer of this money also needs to happen pretty quickly.

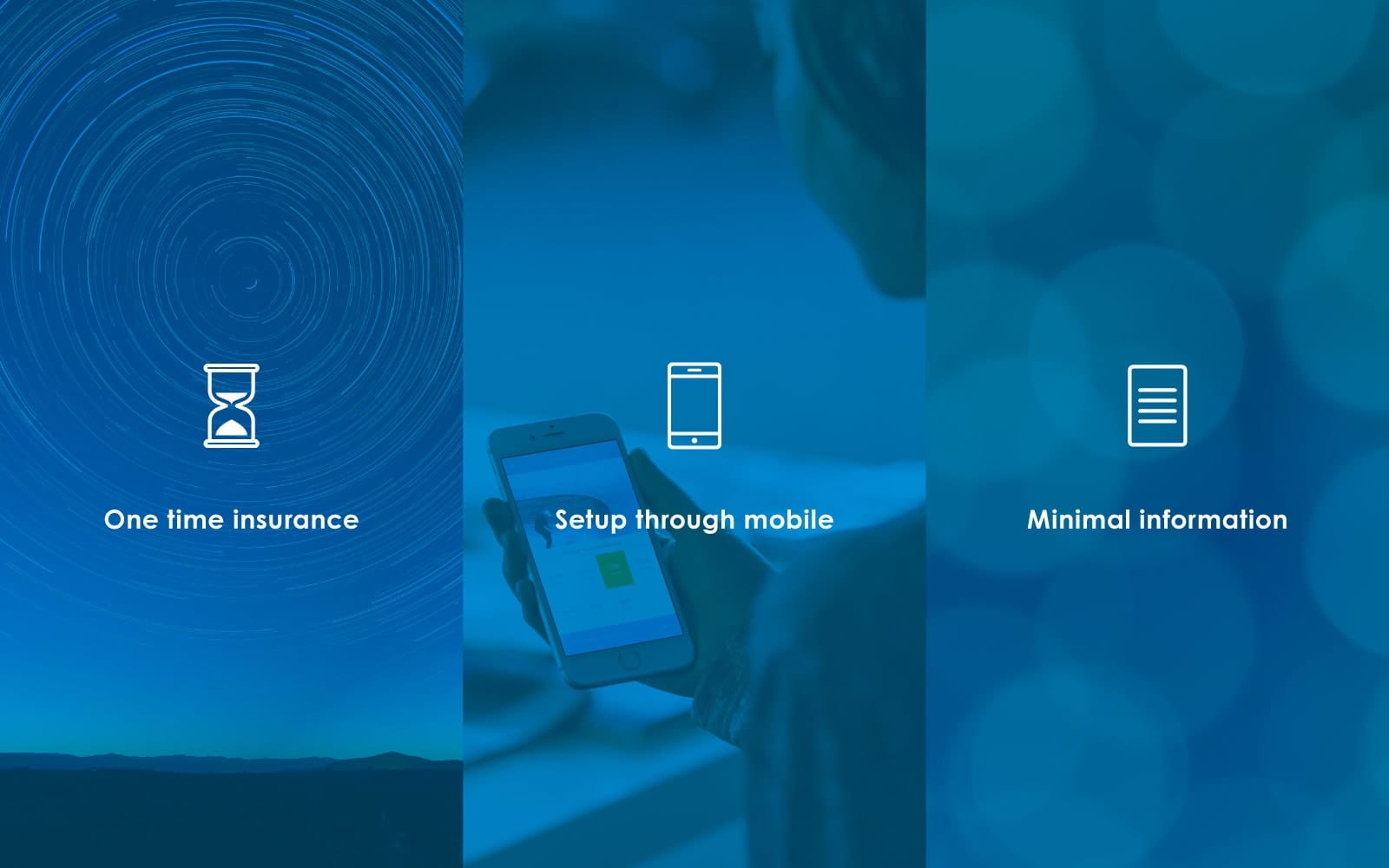

So the on-demand economy, with the help of technology, wants to remedy all these problems. In effect, they aim to make insurance a component that is accessible when the consumer requires it, and pays as per his/her use of the component. How?

Well, mobile technology obviously plays a big role when it comes to access ‘anywhere and everywhere’. With the help of a beautiful mobile interface, customers can begin surfing one of these on-demand services, and the model then goes as follows:

Customers enter their details and other such, creating an account in a jiffy.

They then proceed to choose the items they wish to insure, and add details about them.

Then, policies based on their choices will appear. The customer will now choose a policy the fits their needs the best.

After policy selection, a certain premium will be calculated by the service, which the insurer has to pay as per their model. These payments will mostly be regular and time-bound.

Here’s where the agent comes in. Once the insured item is lost, stolen, damaged and so on, all the customer needs to do is notify the service via the app. The agent will get the claims request on a similar interface.

The agent will then be dispatched instantly to visit and verify the claim: this works through an on-site inspection, and a documents inspection to see if everything is in order.

The claim amount is then given to the customer via the same app.

Sounds pretty nifty right?

Well, there are already a few companies that are dabbling with this, so let’s just take a casual look at them.

“Protect just the things you want – exactly when you want – entirely from your phone. Now available in Australia and the UK. Coming to the US in 2017.”

Trov’s landing page promises this in extremely simple, upfront terms. The model is the same as the one detailed about, where you swipe seamlessly to add items, purchase a policy with premium rate, file a claim and get your money back – all in one app.

Trov promises insurance on individual items, which makes an app necessary to track all the claims and relinquish funds. The insurance can be turned on and off when needed, which is a pleasant alternative for other, rather expensive annual policies.

Trov offers on-demand insurance policies in order to preserve your own assets (computer, smartphone, TV, bicycles, musical instruments, sports equipment). The complaints can be handled in the same way: even with a chat in real time.

Trov has $45 million in new capital to expand its operations, thanks to a Series D funding round led by Munich Re / HSB Ventures. The round brings Trov’s total funding to just over $85 million.

On-demand insurance provider Trov has $45 million in new capital to expand its operations (a boost this April) thanks to a Series D funding round led by Munich Re / HSB Ventures. The round brings Trov’s total funding to just over $85 million.

All of Trov’s Series C investors (Oak HC/FT, Suncorp Group, Guidewire and Anthemis) also participated in the latest round along with one of Japan’s major insurers, Sompo Holdings. This will bring Trov to Japan too!

Another famous name in the realm of InsurTech is Slice Labs. It is already helping companies such as Uber and AirBnB, and aims to eliminate insurance concerns specifically for on-demand companies – truly in the spirit of the on-demand world.

They also provide intensive features such as:

On-demand customized commercial insurance policy purchased via app or online

Primary insurance – no requirement to report claims to another insurer

Commercial liability coverage limit of $2,000,000

Full replacement cost coverage for the home, other structures and contents

No limit to the number of covered properties

Manage coverage, claims and notifications in the app

It caters to the on-demand economy because of the fleeting, vulnerable nature of on-demand transactions – where trust is the primary indicator of doing business in the first place! The co-founder, Ernest Hursh, also declared that Slice was founded since many people working in the on-demand economy do not realize their risk and the fact that they’re simply not covered through conventional means – and aims to level the playing field for them.

Contact Us

Contact UsTeam Up With Us Today For An Unforgettable Service Experience

Book Free Consultation

Book Free Consultation